The year 2008 marked a significant downturn for the United States economy, as it grappled with one of the most severe financial crises since the Great Depression. A confluence of factors, including the bursting of the housing bubble, lax lending standards, complex financial instruments, and a global credit crunch, culminated in a perfect storm that reverberated throughout the nation's economy, impacting millions of individuals and businesses.

At the heart of the crisis was the housing market collapse, fueled by the proliferation of subprime mortgages and the subsequent wave of foreclosures. For years leading up to 2008, lenders had been extending mortgages to borrowers with poor credit histories or insufficient income, often with adjustable interest rates that ballooned over time. This unsustainable lending practice resulted in a glut of overvalued properties and a sharp decline in home prices when borrowers defaulted on their loans.

The fallout from the housing market collapse spread rapidly throughout the financial system, as banks and financial institutions found themselves holding vast quantities of toxic assets tied to subprime mortgages. These assets, bundled into complex securities and sold to investors around the world, rapidly lost value as the housing market deteriorated, triggering massive losses for financial institutions and investors alike.

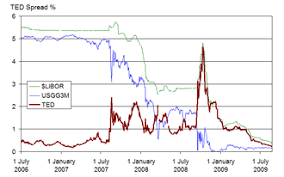

The crisis deepened in September 2008 with the collapse of Lehman Brothers, one of the largest investment banks in the United States. The failure of Lehman Brothers sent shockwaves through the global financial system, causing widespread panic and a loss of confidence in the stability of financial institutions. Credit markets froze, making it difficult for businesses to obtain financing and for consumers to access credit, further exacerbating the economic downturn.

The impact of the financial crisis was felt across virtually every sector of the economy. Unemployment soared as businesses slashed jobs in response to declining demand and tightening credit conditions. The housing market continued to spiral downward, with home prices plummeting and foreclosure rates reaching record highs. Consumer spending, a key driver of economic growth, contracted as households grappled with declining home values, job losses, and mounting debt.

In response to the worsening economic conditions, the U.S. government took unprecedented steps to stabilize the financial system and stimulate economic activity. The Federal Reserve implemented aggressive monetary policy measures, including slashing interest rates to near-zero and launching large-scale asset purchase programs aimed at injecting liquidity into the financial markets.

Meanwhile, Congress passed the Troubled Asset Relief Program (TARP), authorizing the government to purchase troubled assets from financial institutions and provide capital injections to stabilize the banking sector. The passage of TARP was met with controversy and public outcry over the use of taxpayer funds to bail out Wall Street firms deemed responsible for the crisis.

Despite these efforts, the road to recovery was long and arduous. The U.S. economy contracted sharply in 2008 and 2009, marking the onset of the Great Recession, the most severe economic downturn since the 1930s. It would take years for the economy to fully recover from the depths of the crisis, with lingering effects felt in the form of sluggish growth, elevated unemployment, and ongoing challenges in the housing market.

The 2008 financial crisis served as a sobering reminder of the inherent vulnerabilities and interconnectedness of the global financial system. It prompted a reevaluation of regulatory oversight and risk management practices, as policymakers sought to prevent a recurrence of similar crises in the future.